Submitted by QTR’s Fringe Finance

To most of my readers, the move in markets today won’t be much of a surprise. In fact, a couple of the names I talked about over the last week or two (and here) are actually green in today’s blood red tape.

For the most part, I’ve already explained why I think markets could be set up for a much bigger move lower. I detailed this in both my March market review and my piece explaining why I think the next crash could very well be different from those of days past and could “break the brain” of market participants: This Next Market Crash Will Break Our Fragile Brains.

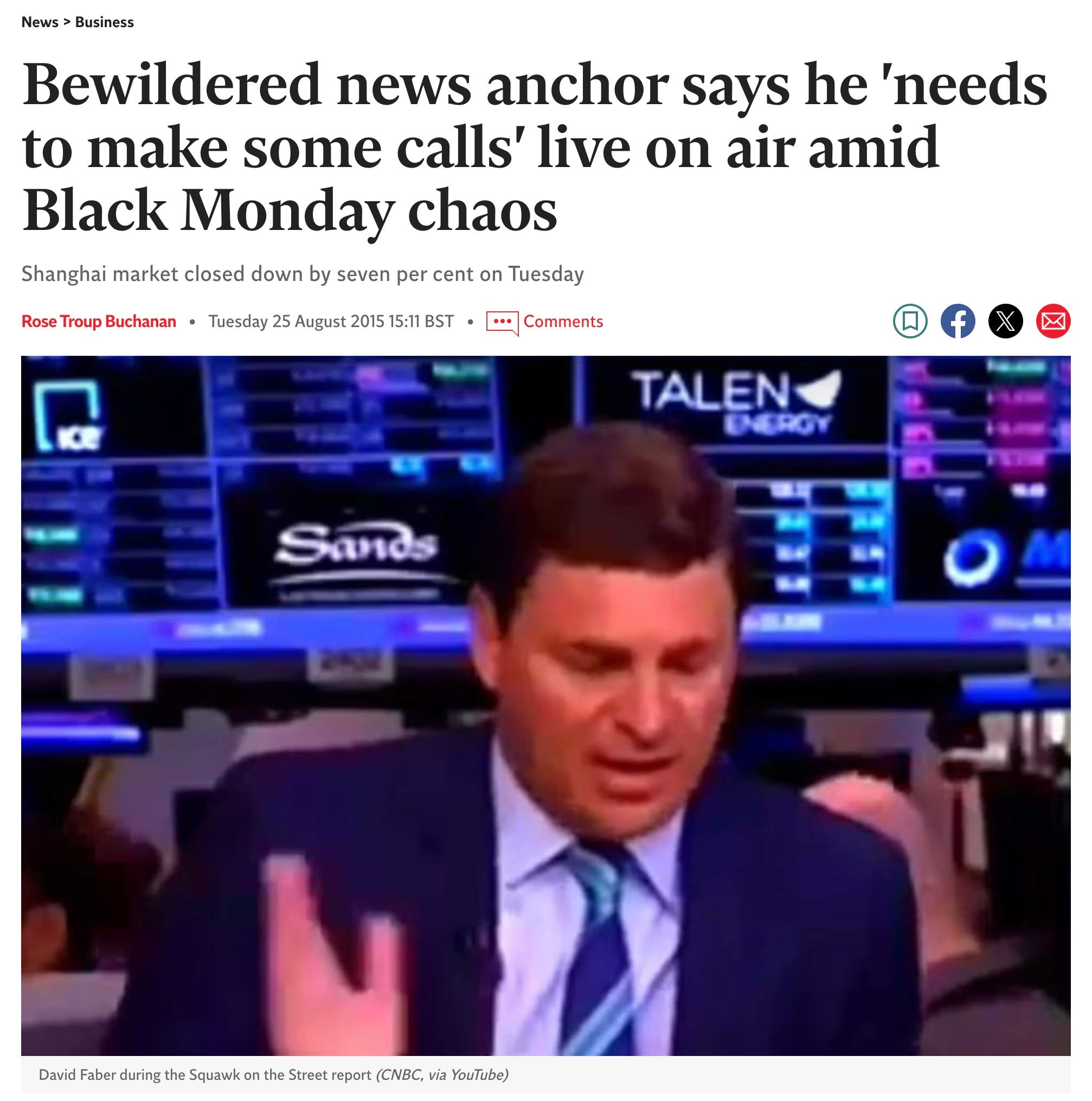

I wasn’t going to write a piece midday today until I turned on the television and, despite the best efforts of David Faber to inject some semblance of reality onto CNBC guests, watched portfolio managers justify paying 26x to 40x earnings for tech stocks they said are “on sale”. Thank God I hadn’t eaten lunch yet, or I may have heaved.

So here’s my quick take on where we stand today and what I’ll be watching for to try and denote some type of overall market bottom in the future.

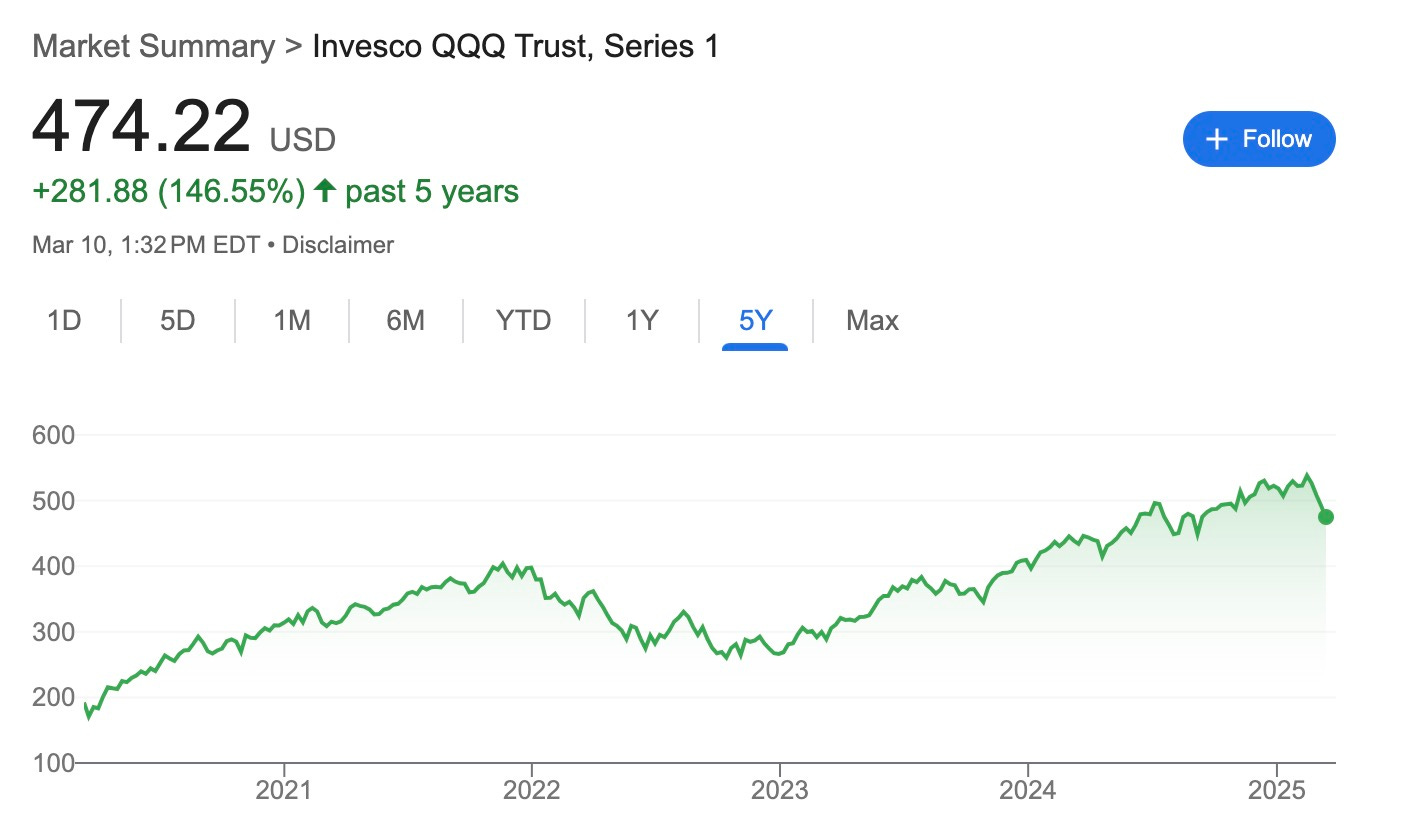

First, let’s keep our bearings about us. While the NASDAQ is down more than 3% today, it is still up more than 140% over the last five years.

Those are astonishing returns that, in my opinion, have been fueled by insanely euphoric expectations, arrogance, hubris, a relentless passive bid as a result of Covid liquidity, and weaponized gamma in the options market.

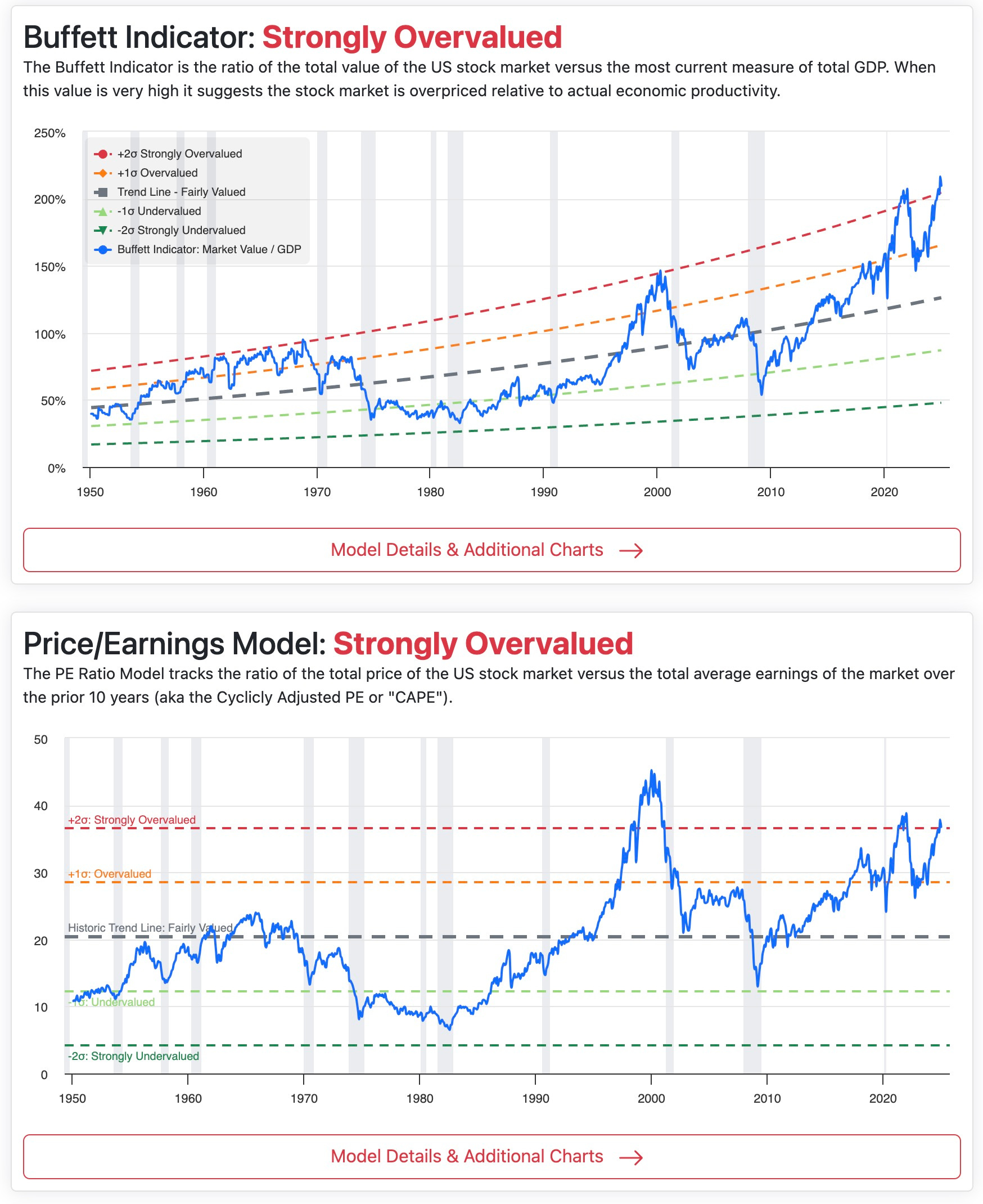

It was a combination of these three things, in my opinion, that led us to far overshoot the euphoria mark on pretty much all valuation metrics. Which is how we got here:

Today when I turned on CNBC, I actually saw David Faber doing a great job of trying to keep some semblance of reality in the air as multiple guests came on and tried to make the ridiculous argument that the tech bullshit they have stuffed their portfolios with at all time highs is somehow “on sale” or “cheap” with names like Apple, Microsoft, and Nvidia still sporting price-to-earnings ratios between 26x and 40x.

“Just take a long-term view,” one of the analysts said today, telling David Faber he was directing his trading team to buy more Microsoft while on the air around lunchtime.

Faber actually did a pretty good job trying to paint a picture of the psychology of the market as it stands today. What he said mostly aligns with what I have been saying over the last couple of weeks: that there is a psychological shift taking place deep in the foundations of the market, not only where people are beginning to entertain the idea that we’re entering a bear market, but also simultaneously entertaining the idea of a rotation out of risk-on speculative US technology stocks and into both US industrials and emerging markets—a sentiment that I have been predicting would take place dating all the way back to the beginning of last year. Here’s what I wrote at the beginning of 2024:

2023 was a year marked by insanely aggressive gains in tech and the NASDAQ. Despite higher rates, investors still haven’t shifted their investing outlook from growth to value, and, as shown in the price of commodities, investors still aren’t positioning themselves defensively. This is a rotation that is long overdue, in my opinion.

I feel like with valuations where they are, technology names could wind up seeing a significant pullback in the coming year, while the steady and consistent dividends of utilities and consumer staples could produce a total return for the year that should be able to beat both the S&P and the NASDAQ if I’m correct.

With the Japanese bond market now on the verge of cracking up, Germany not far behind, and the US eventually going to follow suit, it sure does seem like our markets could be on a path for yield curve control and a multiple-years-long stagnant equity market, not unlike what we’ve seen in Japan over the last decade.

“Japan JGB auctions going from terrible to worse: last week saw a dismal 10Y auction with lowest Bid to Cover since 2021 and a spiking tail. And now another terrible 5Y auction, with the lowest Bid to Cover since June 2022,” Zero Hedge wrote late last night, at yields across the curve hit highs. They predict a failed auction soon. Here’s the 40Y blowing out:

Chart: Zero Hedge

In an environment like this, the sentiment would almost definitely benefit emerging markets, value stocks, industrial stocks, and any type of boring blue-chip stock you would’ve seen heralded as a safe play back in the 90s before the notion of value and stock picking in markets was taken out back and pissed on by the Federal Reserve.

But that could all be a long way away, and it’s pretty heavy talk for the market being down barely 10% off its highs. With that being said, the sentiment I’m seeing on financial news and social media isn’t anything near what I would consider capitulation and, therefore, some type of psychological bottom. As far as a bottom for fundamentals, the market could easily get cut in half in here and still not necessarily be “cheap.” I think we all know the Federal Reserve likely won’t let that happen unless a massive deleveraging runs wild and creates a one-off crash event. But let’s say valuations come in 20% to 30% on ‘25 or ‘26 earnings—this would be an area where I would start to also want to gauge psychological sentiment.

To me, psychological sentiment at the bottom literally looks like the “hell is coming” moment Bill Ackman had during Covid. Right now, all these crumb bums that are flapping their gums all day on CNBC are fighting this trend of the market moving lower. It’s just one excuse after the other. “It’s a great opportunity to buy,” they clamor — yeah, with little to no acknowledgment of how overvalued everything is, the potential for the market to move lower, or things like private credit marks and commercial real estate, among other time bombs that may be waiting for the market out there as it sells off.

Everybody today on TV was trying to fight the market. And to some degree, they have to. Most of these people have been on TV every day over the last couple of weeks telling everybody to buy as the market moves lower. And so what other options do they have? Admit they were wrong? That’s never gonna f*cking happen.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

So instead, we get every possible mental gymnastic contortion of reality and bullshit excuse available as to why today is definitely going to be the bottom—at least until tomorrow—and investors who are “savvy enough” to take a long-term view should view this as an opportunity.

Nobody ever asked a question like: What happens if the S&P reverts to an average P/E ratio of 18 times earnings for the next decade? In that case, it doesn’t matter whether you have a one-year, five-year, or 10-year outlook; it’s not an opportune time to buy here. End of story.

But I digress. What I’ll be watching for is when the very same huge-brained analysts on TV today arguing that expensive stocks are “cheap” finally surrender and admit that this market is broken and that “it’s different this time” but only to the downside.

When these people are finally liquidated, and some firms start blowing up — when anchors sh*t their pants and run off the desk on live TV — maybe I’ll start wondering whether or not market psychology has changed.

If some recurring guests on CNBC never get invited back or just outright disappear mysteriously, then I’ll start paying attention to psychological sentiment. And when the crowd that has been crowing for you to buy the dips for the last five years has their very own “hell is coming” moment and outright throws their hands up in the air to tell us that everything they’ve ever known about finance and markets has been proven wrong…well, that’ll be the time I’ll start wondering if psychological sentiment has changed.

Of course, I’m being half hyperbolic, but you get the idea. When the “hell is coming” moment happened during Covid, it felt like serious business. It felt like Ackman could be 100% right, and the unknown of the pandemic could actually be the end of the world. Looking back on it now, it’s really easy to say that marked the bottom. Keep this in mind the next time you feel scared shitless about the market in the present moment. Then ask yourself, how will I feel five years from now?

As for me right now, all I have to do is look at a six-month chart or a 12-month chart than NASDAQ as a friendly reminder that this market is still green for most participants that have entered it over the last year. And to me, that doesn’t sound like the kind of environment where capitulation or a bottom, even a temporary one, is taking place.

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. Assume any and all numbers in this piece are wrong and make sure you check them yourself. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Loading…